Buying your very first home is an exciting time – but it can feel a little overwhelming. Don’t worry, Uplend is here to help with everything you need to bring your dream home to life – whether that’s saving for your deposit, understanding how much you can borrow or what your repayments might look like.

They’ll also help you understand what to consider when looking for a property, the next steps once you’ve found one and what to expect during the settlement process

Generally, if you’re able to offer a larger deposit, say, 20% of the property value, you could save by not having to pay Lender’s Mortgage Insurance (LMI). However, if saving a deposit of this size is not achievable, it’s common for home loan providers to offer lower deposit options of up to 95% of the property value, but you would generally need to pay LMI.

There may be other upfront costs you need to consider including:

Application and valuation fees

Stamp duty

Government fees such as mortgage registration, title search and transfer fees

Conveyancing and legal costs

Site costs, if you’re building a new home

Building and pest inspections

Home insurance before settlement, and possibly contents insurance when you move in

There may also be ongoing costs once you move into your new home, including strata fees, utility fees (water, gas and electricity) and council rates. You’ll be responsible for them from settlement.

There are many pathways you can take when saving for your first deposit. The one best suited to you depends on your financial situation

LMI is a one-off fee charged by a home loan provider. It’s usually needed when you have a deposit of less than 20% and insures the home loan provider in case of non-repayment by the borrower. The amount of LMI varies depending on the amount borrowed and the size of the deposit that you are able to offer. There may be the option to include the LMI fee into your home loan amount, allowing you to pay it off over the life of your home loan.

The FHSS Scheme allows you to save money for a first home inside your superannuation fund. This could help first home buyers save faster with the concessional tax treatment within super. To find out more, search ‘ATO First Home Super Saver Scheme’ online.

If you’re buying or building your first home, you may be eligible for a grant or stamp duty concession to help with your property purchase. Most states and territories have their own scheme and the offers, qualification criteria and processes for applying vary accordingly.

To check which grants apply in your area, visit your relevant state or territory information at firsthome.gov.au

Family Pledge allows for a family member to guarantee part of your home loan - while having the peace of mind to set the guaranteed amount. This option helps reduce the loan to value ratio (LVR) or possibly eliminates the need to pay Lenders Mortgage Insurance.

When buying a home, knowing your borrowing potential and repayment costs is a great place to start. You can then work out a budget that includes your everyday living expenses and other financial commitments. Remember, if you need a hand, we’re here to help.

Assess your current obligations and consider whether you can pay these off along with a home loan. Include any credit cards, student loan debts or store cards you may have.

Consider how much of your savings you could comfortably use as a deposit. If you’re buying a property that you are going to live in, home loan providers often accept deposits starting from 5% of the purchase price.

Determine what you can afford to repay per week, fortnight or month, and then work out your budget based on your pay cycle.

Consider how long you’ve been in your job. Make sure you’ve cleared any probation periods and you’re in a financially stable position.

How much can you give up? Ensure you don’t overcommit yourself and include everyday expenses like groceries, transport and entertainment in your calculations.

If you’re thinking of having a family, you should consider what impact children could have on your budget and ability to repay a home loan.

Also referred to as ‘pre-approval’ or ‘approval in principle’, conditional approval is an obligation-free way to estimate how much you could afford to borrow before you make an offer on a property.

Once given, conditional approval is valid for 90 days from the approval date. If you don’t find a property within this period, you may renew for another 90 days by confirming your financial circumstances haven’t changed.

‘Conditional approval’ is our way of approving you for a loan before giving it to you. It’s based on certain conditions being met when we give ‘unconditional approval’. The conditions could range from information about your current financial position to a satisfactory valuation for the proposed property.

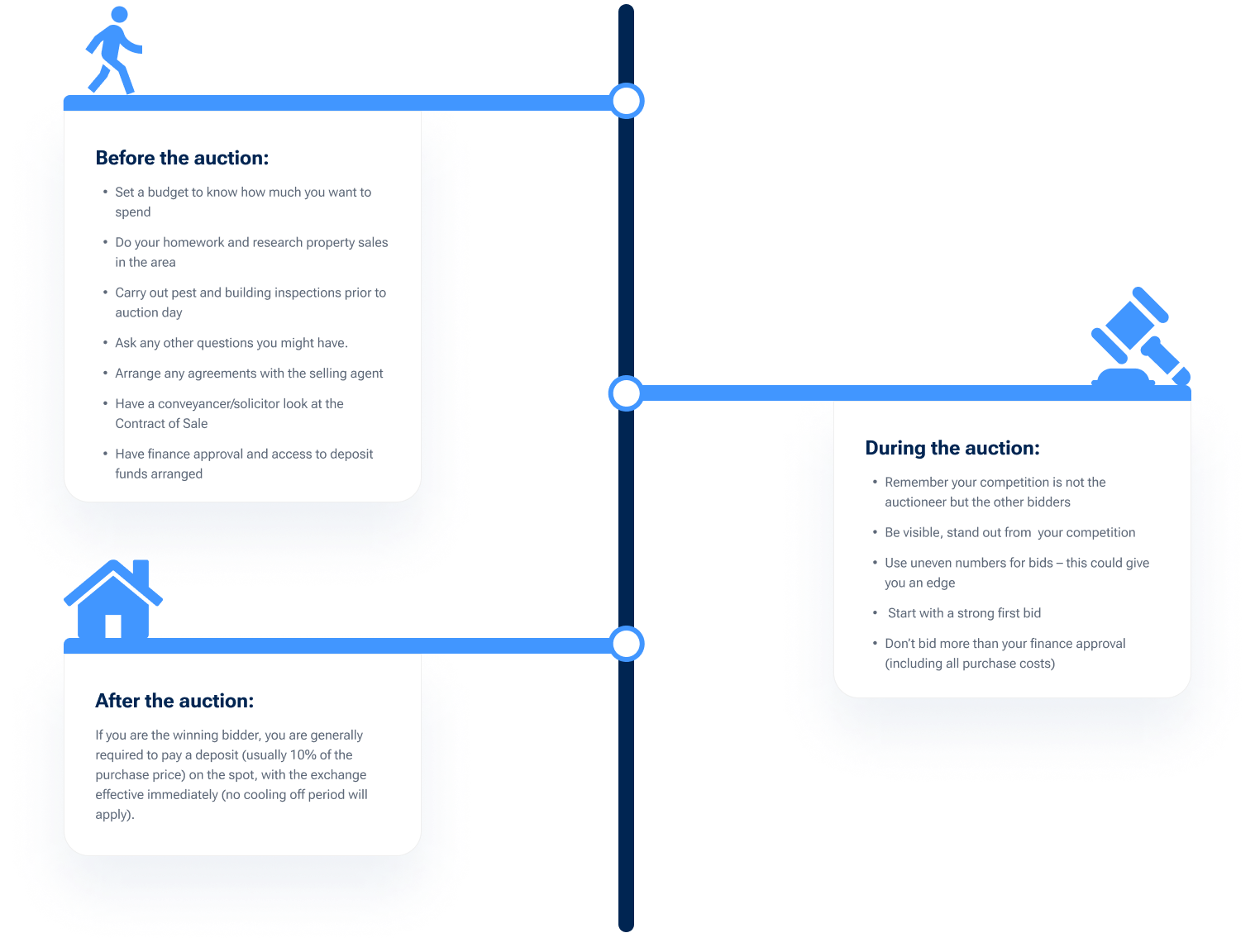

Finally found that perfect property? Before you rush to the auction or make an offer, be sure to do your final checks and ask your Lending Manager for a Property Report* so you can be completely confident with your decision.

There’s a wide range of home loan options offering you a mix of flexibility, certainty and peace of mind. Consider whether you would prefer a variable or fixed interest rate – or a bit of both. Your Lending Manager can help you understand which option is best for you.

Know how much you can spend before you start house hunting. Get a conditional approval letter from your home loan provider.

Get online alerts about properties up for sale where you’d like to buy using popular websites like realestate.com.au or domain.com.au

.png)

There’s nothing worse than feeling like you overspent. Buying at the right price is the cornerstone of any successful purchase.

Don’t judge a house by its paint job. Examine what lies underneath. Check for structural damage, sagging ceilings, water stains on walls, smell of damp, fine cracks on walls, evidence of mould.

Speak with a local real estate agent as they’re equipped with a wealth of information, from up-and-coming suburbs to the sale prices of properties in your desired area.

Don’t be afraid to negotiate the price with the seller. You could save a significant amount and might not need to borrow as much.

Know how much you can spend before you start house hunting. Get a conditional approval letter from your home loan provider.

There are some key steps you may want to cover off when you’re preparing to purchase:

Make sure your legal rights are protected in respect of the purchase.

Investigate issues affecting the property, such as local authority plans in the area, or environmental risks, such as flooding.

Prepare the legal documents that ensure the property is transferred into your name once the sale is completed.

Ensure the settlement process stays on-track by coordinating the legal representatives of the vendor and any home loan providers.

Conduct property searches at your instruction. These cover things you may not know about the property from simply viewing it – including title and strata searches.

Tell you about the conditions of the sale.

Help you understand cooling off periods. Most states have a cooling off period, except for sales at auction, which generally do not have any cooling off period.

Double-check your chosen area’s zoning. Make sure it won’t be impacted by proposed developments that may affect you long term. You may also need to identify the flood or fire risk for a property. This information can generally be found on the local council website.

These will help ensure the property is in the condition specified in the strata report and/or identify hidden contract issues in the case of structural damage or termites. Talk to your real estate agent to arrange these inspections.

Your Lending Manager can discuss some of the options available to you and advise of any insurance you may require prior to settlement. There are different types of insurances depending on your needs, so be sure to consider what’s right for you.

Ensure a copy of the Contract has been reviewed by your solicitor/conveyancer

From making an offer to finalising your home loan and the settlement process – the final stages of buying a home can be confusing. That’s why it’s a good idea to ask a solicitor or conveyancer to help you navigate this part of the process.

Once you’re ready to make an offer, it’s time to determine which type of sale yours will be.

If you’re interested in purchasing the home, contact the seller’s real estate agent after the open house. You may want to make a verbal offer and set any conditions of the offer for the real estate agent to present to the vendor.

Find out whether there’s any competition by asking the real estate agent whether any offers have been made. It’s also good to ask how soon the vendor is hoping for settlement as it could help you to negotiate a price.

Find out from the agent as much as you can about the vendor’s situation. If the vendor has already purchased elsewhere, then they may be in a hurry, so they could consider dropping the price.

It’s important to understand the vendor may not accept your first offer and you may need to make several offers before reaching final agreement.

Don’t start with your highest offer. You may not know what offers have already come in, if any. You’ll also be left with no room to negotiate

Try not to show the agent how much you like a property. Remember they are working for the seller. If they detect your enthusiasm they may try and drive a higher price.

If you’re buying through a private treaty sale you are usually initially required to pay a holding deposit, which in turn will initiate a cooling off period, during which the seller cannot accept another offer from a different buyer

Once your offer has been accepted, we will need to finalise your home loan application and complete a property valuation. There are a number of documents required to formalise your loan approval and make a formal loan offer to you. Your Lending Manager will be able to help you understand this process and finalise your home loan application.

You’re on the home stretch! Property settlement is the legal process of transferring ownership of the property from the seller to the buyer. It’s facilitated by your legal and financial representatives and those of the seller.

The ‘settlement period’ (when you sign the contract to when settlement is finalised) is generally 6 weeks. However, it can vary from 4-12 weeks, depending on the agreement between you and the seller

Settlement day is the day you become the owner of your new property. Generally, the legal and financial representatives will meet on behalf of you and the seller to finalise the transfer of property ownership.

Once that’s done, all that’s left to do is pick up the keys!

By dividing your monthly payments into two and paying fortnightly, you’ll squeeze in one extra repayment each year. Over time, that will reduce the amount of interest you could potentially pay

If you are on a variable rate home loan and your minimum monthly repayments drop due to interest rates being reduced, you may want to consider maintaining your existing repayments. It could help you pay off your home loan sooner by reducing the amount of interest you pay.

Consider making your savings work harder, by ‘offsetting’ them against your home loan. An interest offset account will give you the flexibility of accessing your money when you need to, with the benefit of paying off your home loan sooner.

Think of your equity as a deposit for your next home or savings, not something to spend on holidays or entertainment. If you’re having trouble managing debt, speak to a financial advisor and contact your home loan provider about your loan options.

Making higher than minimum repayments can make a big difference. However, you need to ask your home loan provider if this is possible as there might be conditions and/or fees involved, particularly if you have a fixed-rate loan. Some fees, such as fixed-rate break costs, can be substantial.

You may also wish to increase repayments with any pay rise and allocate your annual bonus, tax return or other windfalls to your home loan.

Consider arranging a home loan health check with your Lending Manager every few years. You’re likely to have a home loan for many years and your circumstances or needs could change during that time. Contact your Lending Manager to see whether you can arrange a better deal.

Uplend is a trusted mortgage broking firm, dedicated to helping Australians secure the best home loans for their property purchases and refinances.